How Mental Health Affects Retirement Financial Preparation

The Importance of Mental Health in Retirement Planning

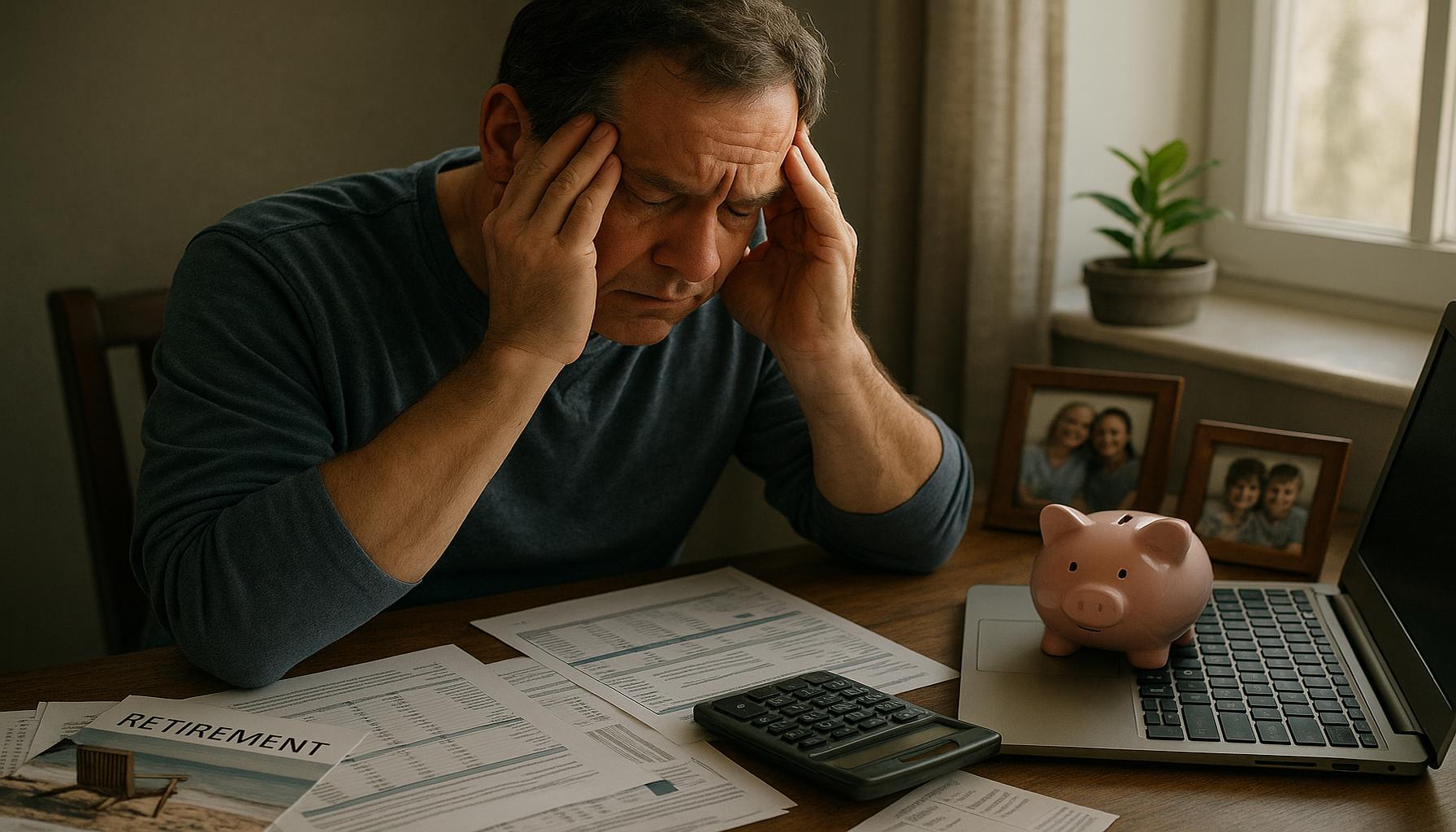

Planning for retirement is often viewed only through a financial lens, focusing on savings, investments, and budgeting. However, the aspect of mental health is a critical component that can significantly influence how individuals prepare for and navigate this important life transition. Understanding how mental health interacts with financial readiness can enable individuals to create a more holistic retirement plan.

Several factors contribute to the relationship between mental health and financial readiness, including:

- Anxiety about the future: Many individuals experience stress related to financial security as they approach retirement age. This anxiety can lead to indecision or hasty financial choices, such as withdrawing funds prematurely or not investing wisely. For example, a person who worries about outliving their savings may choose overly conservative investment strategies that yield low returns, ultimately compromising their long-term financial health.

- Depression: Mental health struggles such as depression can rob individuals of motivation, making it difficult for them to engage in proactive retirement planning. This could manifest in neglecting to review their retirement accounts or not seeking necessary financial advice, which could otherwise enhance their savings efforts. Imagine someone who is feeling hopeless regarding their future and therefore procrastinates on setting up their retirement fund altogether, leading to a lack of preparedness.

- Overconfidence: Sometimes, individuals may enter retirement planning with an overly optimistic view of their financial situation. This overconfidence can result in underestimating the actual costs of living in retirement, including healthcare and everyday expenses. For instance, a person might believe that they can live off of their current income without considering inflation or unexpected costs, ultimately leaving them financially vulnerable.

Mental health challenges can also complicate the already intricate process of financial planning in various ways:

- Difficulty in understanding financial concepts: High levels of stress and anxiety can impair cognitive functions, making it hard for individuals to grasp complex financial instruments like annuities or stocks. This lack of understanding can lead to poor investment choices that jeopardize long-term savings.

- Poor spending habits: Those struggling with mental health issues may engage in impulsive spending as a form of coping or escapism, undermining their ability to save for retirement effectively. For example, someone may splurge on vacations or luxury items to momentarily escape feelings of anxiety, resulting in depleted savings when they should be focusing on building their nest egg.

- Reduced social support: Isolation from mental health challenges can limit an individual’s access to crucial resources and advice needed for sound financial planning. Without family or friends to discuss financial decisions with, they may miss out on valuable perspectives or insights that could aid their journey towards retirement.

Recognizing the interconnectedness of mental health and financial planning is vital. By understanding how mental health influences financial preparedness, individuals can adopt strategies to enhance both their financial stability and their emotional well-being. For example, seeking professional help for mental health issues or joining a support group can create an environment conducive to making informed and deliberate financial decisions, empowering individuals to take control of their retirement journey and enjoy their golden years with peace of mind.

DISCOVER MORE: Click here to learn how to apply easily

Understanding the Mental Health-Financial Connection

To grasp the profound effects that mental health has on retirement financial preparation, it’s essential to first identify and unpack specific mental health issues that commonly arise during the transition into retirement. As individuals approach this significant life change, both their emotional state and decision-making capacity can be profoundly impacted. Let’s explore how different aspects of mental health can shape one’s financial planning.

Anxiety’s Financial Implications

Anxiety often becomes a constant companion as individuals move closer to retirement. This anxiety can stem from multiple sources, including worries about living expenses, healthcare costs, and the potential for economic downturns. Such concerns can cloud judgment, leading to either over-cautious financial strategies or reckless ones. For example, someone paralyzed by the fear of not having enough may opt to keep their funds in low-yield savings accounts, foregoing potentially higher returns from diversified investment portfolios. In such cases, underlying anxiety directly affects decision-making and can limit financial growth opportunities.

Impact of Depression on Financial Responsibilities

Depression can create a cloud of hopelessness that affects everyday motivation, significantly complicating financial planning. Individuals experiencing depression may find it challenging to engage with their retirement savings actively. This can include failing to regularly review accounts, ignoring important deadlines, or avoiding seeking out professional financial advice. Imagine someone who has stopped contributing to their retirement 401(k) because they feel overwhelmed by the sheer weight of their emotions. This neglect ultimately leads to a missed opportunity for building a secure financial future.

Overconfidence and its Downfalls

Interestingly, mental health also manifests in the form of overconfidence, where individuals may underestimate the financial challenges that lie ahead. This tendency often leads to unrealistic assumptions about their retirement lifestyle, such as assuming that maintaining current living expenses will suffice without accounting for inflation or unforeseen events like medical emergencies. Overconfidence can result in setting aside an insufficient amount for retirement, which can ultimately leave individuals struggling to meet their needs in later years. Here’s where a detailed financial projection, considering all potential expenses, becomes essential. Underestimating costs due to inflated confidence can jeopardize financial security.

Coping Mechanisms and Their Effects on Spending

People grappling with mental health challenges often resort to unhealthy coping mechanisms, which can include impulsive spending. For instance, someone dealing with anxiety may indulge in retail therapy as a temporary escape, leading to significant disruptions in their savings plan. These impulsive financial decisions can erode the very foundation of retirement plans, leaving insufficient funds when the individual needs them the most.

As we can see, mental health issues directly influence various aspects of financial preparation for retirement. Recognizing these connections enables individuals to approach retirement planning with greater awareness of their emotional state and its potential repercussions. By addressing mental health proactively, they can enhance both their financial well-being and their overall quality of life, ensuring a brighter, more secure future in retirement.

DISCOVER MORE: Click here to learn how to apply

The Interplay Between Mental Health, Financial Planning, and Retirement Security

Continuing our exploration of how mental health influences retirement financial preparation, we must consider not just the immediate emotional impacts but also the long-term behaviors and attitudes that may emerge as individuals navigate this life transition. Recognizing these patterns can empower individuals to approach financial planning with greater clarity and intentionality.

Fear of Change and Financial Paralysis

The transition into retirement represents a significant life change, and with it, many face a profound fear of the unknown. This fear can lead to decision-making paralysis, where individuals are so overwhelmed by the possibilities that they refrain from taking necessary actions. For instance, someone nearing retirement may hesitate to reallocate their investments or streamline their budgets, fearing that any change will exacerbate the volatility of their financial future. This paralysis can prevent proactive measures, such as maximizing contributions to retirement accounts or seeking more favorable investment options, ultimately stalling financial progress.

The Role of Support Networks

The lack of a robust support network can also exacerbate mental health challenges, affecting financial planning. Individuals who do not have strong familial or community ties may struggle more with mental health issues and experience increased feelings of isolation. This isolation can hinder the ability to talk openly about finances, seek help, or collaborate on planning strategies. When people feel supported, they are better equipped to confront their mental and emotional obstacles, making it easier to address financial concerns head-on. Building a trustworthy support network can be crucial in bolstering both emotional resilience and financial discipline.

Retirement Dreams vs. Reality: A Psychological Tug-of-War

Retirement dreams often include travel, hobbies, and spending quality time with family. However, when mental health struggles come into play, the gap between these aspirations and financial realities can create distress. Individuals may feel guilty for not being able to afford or pursue their desired retirement lifestyle, leading to further anxiety or depression. If someone has anticipated a luxurious retirement but is faced with mounting healthcare costs or inadequate savings, this cognitive dissonance can be psychologically damaging, making it essential to align dreams with actionable financial plans. Realistic goal-setting, coupled with a clear understanding of one’s financial situation, can help bridge this gap.

The Importance of Professional Guidance

With the complexities tied to mental health and financial planning, seeking professional guidance can provide crucial support. Certified financial planners can offer insights that account for emotional considerations, aligning financial strategies with personal mental health. For instance, a financial planner might suggest creating a flexible budget that accounts for both potential medical expenses and discretionary spending on leisure activities, providing peace of mind while adhering to financial goals. Professional guidance can demystify retirement planning, reducing the anxiety that often accompanies financial decisions and empowering individuals to take charge of their financial futures.

As we delve deeper into these interconnected elements, it becomes increasingly clear that addressing mental health is not only about improving emotional well-being; it’s also a vital component of ensuring sound financial preparation for retirement. Understanding and integrating this knowledge into financial planning can pave the way for a more stable and fulfilling retirement experience.

DIVE DEEPER: Click here to learn how to apply

Conclusion: The Integral Link Between Mental Health and Financial Planning for Retirement

In summary, the interplay between mental health and financial preparation for retirement is profound and multifaceted. Individuals must recognize that their emotional well-being significantly influences their ability to make sound financial decisions. Fear, anxiety, and isolation can stunt proactive financial behaviors, such as investing wisely or adjusting spending plans, ultimately threatening long-term stability. Conversely, an understanding of this connection empowers individuals to confront these fears and actively engage in planning their financial futures.

Having a support network is crucial in overcoming mental health challenges related to financial planning. Friends, family, or professionals can provide encouragement and accountability, creating a safe space for discussing financial concerns and sharing insights. Furthermore, realistic goal-setting aligned with available resources helps bridge the gap between aspirations and financial realities, leading to a more harmonious retirement experience.

Lastly, seeking professional guidance can alleviate many complexities involved in retirement planning. Financial advisors who consider emotional factors can tailor plans that not only meet financial goals but also address mental health needs. This holistic approach cultivates resilience and confidence, empowering individuals to thrive during their retirement years.

Ultimately, acknowledging and addressing the impact of mental health on financial planning is essential for a fulfilling and secure retirement. By prioritizing emotional well-being and utilizing available resources, individuals can prepare for a future that aligns with both their financial and personal aspirations.

Related posts:

The Impacts of the Social Security Reform on Future Pensions

How Changes in Retirement Policies in the US Are Impacting Workers' Financial Future

The Role of Financial Technologies in Retirement Finance Management

The Role of Technology in Managing Personal Finances during Retirement

Demystifying 401(k) Plans: What You Need to Know to Maximize Your Benefits

The Importance of Investment Diversification in Building a Retirement Fund

Linda Carter is a writer and financial expert specializing in personal finance and financial planning. With extensive experience helping individuals achieve financial stability and make informed decisions, Linda shares her knowledge on our platform. Her goal is to empower readers with practical advice and strategies for financial success.